What Is the Difference Between Crypto and the RBI’s Digital Rupee (e₹)?

The difference between crypto and the RBI’s Digital Rupee (e₹) is not just technical – it is philosophical. The e₹ is India’s Central Bank Digital Currency (CBDC), issued and fully controlled by the Reserve Bank of India, backed by the government, and designated as legal tender. Private cryptocurrencies like Bitcoin and Ethereum are decentralised, issued by no authority, backed by nothing except code and collective trust, and explicitly not legal tender in India. The two look superficially similar – both are digital, both run on some form of ledger – but they represent opposite ends of the monetary spectrum. This article compares them across every dimension that matters for Indian users: issuer, supply, privacy, legal status, purpose, and what each can actually be used for.

What Is the RBI’s Digital Rupee (e₹)?

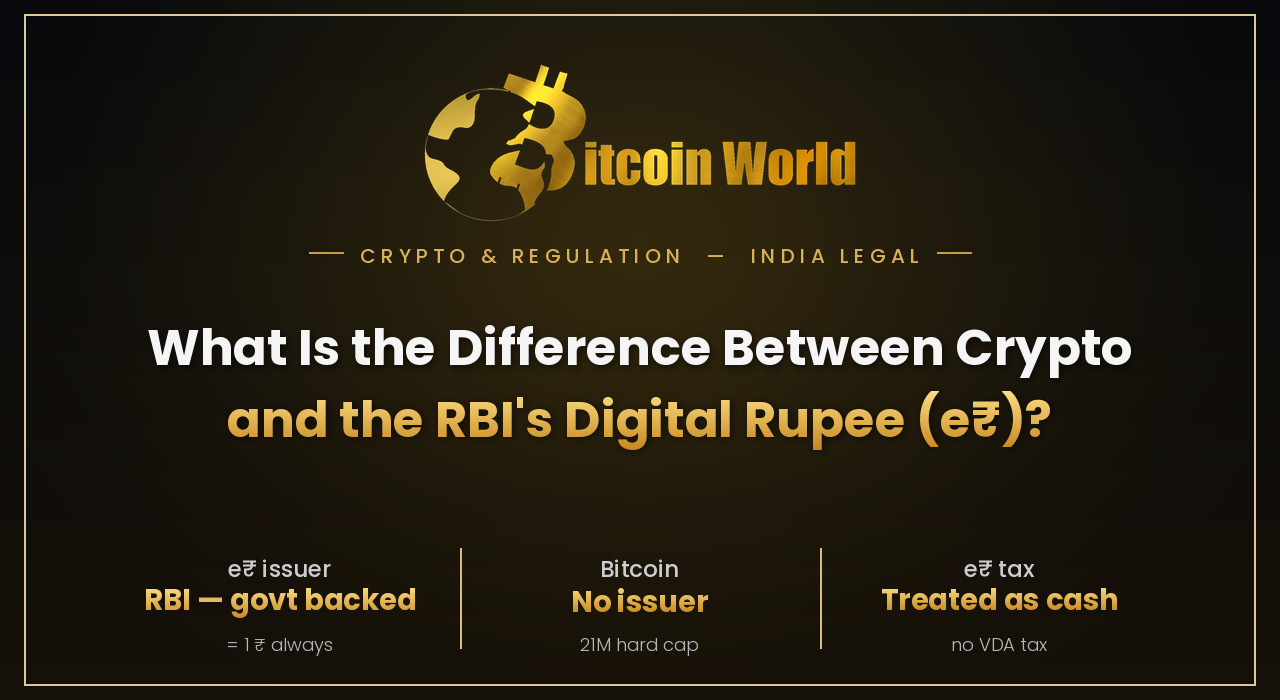

The RBI’s Digital Rupee (e₹) is India’s official Central Bank Digital Currency – a digital form of the Indian Rupee issued directly by the Reserve Bank of India.

- Issuer: The Reserve Bank of India – the same authority that issues paper currency notes.

- Legal tender: The e₹ is designated legal tender – merchants are obligated to accept it just as they accept physical rupees.

- Value: 1 e₹ = 1 ₹ – it is not a separate asset; it is a digital representation of the rupee itself.

- Supply: Issued and controlled by the RBI; supply is unlimited and adjustable by monetary policy, just like cash.

- Two variants: The retail e₹ (e₹-R) for consumer payments; the wholesale e₹ (e₹-W) for interbank and institutional settlement.

- Scale in 2026: By April 2026, the RBI was routing portions of India’s ₹6.6 lakh crore (~$80 billion) welfare payment system through the e₹ in pilot programs across Maharashtra and Gujarat, with BRICS economy integration under active development.

How Is Private Crypto Like Bitcoin Fundamentally Different From the e₹?

Crypto and the Digital Rupee diverge across every foundational dimension.

| Dimension | Bitcoin / Private Crypto | RBI Digital Rupee (e₹) |

| Issuer | No issuer – code and network | Reserve Bank of India |

| Legal tender | No – cannot be demanded as payment | Yes – must be accepted |

| Supply | Fixed (Bitcoin: 21M cap) or pre-defined | Unlimited – RBI controls |

| Control | Decentralised – no single authority | Fully centralised – RBI |

| Blockchain type | Public, permissionless | Private, permissioned |

| Privacy | Pseudonymous – publicly visible on-chain | Fully traceable by RBI and government |

| Volatility | Highly volatile | Stable – equals 1 ₹ |

| Tax treatment | VDA – 30% gain tax, 1% TDS | Treated as cash – no separate crypto tax |

| Backing | Code, scarcity, network trust | Government of India guarantee |

| Purpose | Store of value, speculation, DeFi | Payments, welfare, monetary policy |

Why Is the Government Promoting the e₹ Alongside Regulating Private Crypto?

The e₹ and private crypto regulation reflect two parallel strategies pursuing the same goal – maintaining monetary sovereignty in a digital economy.

- The RBI’s concern: Private crypto undermines monetary policy transmission, enables capital outflows, and creates financial stability risks outside RBI control.

- The e₹ response: A government-issued digital currency that offers the efficiency of crypto payments – instant, low-cost, digital – without giving up central bank control.

- Complementary not competing (for the government): The government taxes private crypto at 30% to disincentivise speculation while promoting the e₹ for actual payments.

- Competing for the user: From an Indian user’s perspective, the e₹ is a payment tool while Bitcoin is an investment asset – they serve different purposes and are not substitutes.

What Can Each Actually Be Used For in India in 2026?

Practical use cases make the distinction immediately clear for Indian users.

e₹ (Digital Rupee):

- Paying utility bills, school fees, and government services.

- Receiving salary and welfare payments (₹6.6 lakh crore welfare routing via e₹ pilots).

- Merchant payments at shops and online.

- Cross-border BRICS-aligned settlements.

- Cannot be used as investment or savings hedge – it simply equals 1 ₹.

Private crypto (Bitcoin, Ethereum, etc.):

- Holding as a long-term store of value or investment.

- Trading and speculation on registered exchanges.

- DeFi, staking, yield generation.

- Cross-border transfers where banking channels are expensive.

- Cannot be used to legally enforce payment of debts in India.

Frequently Asked Questions

Is the Digital Rupee (e₹) the same as cryptocurrency in India?

No – the Digital Rupee is not cryptocurrency in the commonly understood sense. It is a Central Bank Digital Currency (CBDC) issued and fully controlled by the RBI, designated as legal tender, and equal in value to 1 physical rupee. Private cryptocurrencies like Bitcoin are decentralised, issued by no authority, volatile in price, and not legal tender. The two share the word “digital” but represent opposite monetary philosophies.

Does the Digital Rupee (e₹) attract the 30% crypto tax in India?

No – the e₹ is treated as cash, not as a Virtual Digital Asset under Section 2(47A) of the Income Tax Act 2025. Spending or receiving e₹ is the same as spending or receiving physical rupees – it does not trigger VDA tax obligations. The 30% flat tax and 1% TDS apply only to private VDA transfers, not to transactions in the government-issued digital currency.

Can you invest in the Digital Rupee like Bitcoin in India?

No – the e₹ is a payment instrument, not an investment. It is equivalent to 1 ₹ and does not appreciate in value, cannot be traded for profit, and is not listed on crypto exchanges. Bitcoin and private cryptocurrencies are investment assets whose price fluctuates with market demand; the e₹ is stable by design and backed by the RBI. Using e₹ to “invest” would be equivalent to investing in physical cash.

Conclusion: Why the Crypto vs e₹ Distinction Is Central to Understanding India’s Digital Money Future

The difference between crypto and the RBI’s Digital Rupee is the difference between decentralised money and central bank money – and India in 2026 has made room for both while treating them very differently. The e₹ is legal tender, tax-neutral, and government-controlled; private crypto is a taxed, regulated, speculative asset with no legal tender status. For Indian users, they are not substitutes – the e₹ replaces cash for everyday payments, while private crypto remains an investment class with its own framework, obligations, and risks.

Disclaimer: The information provided is not trading advice, Bitcoinworld.co.in holds no liability for any investments made based on the information provided on this page. We strongly recommend independent research and/or consultation with a qualified professional before making any investment decisions.