A death spiral is something many of us never hope to be trapped in- it means the loss of massive amounts of capital, and the rapid devaluation of tokens that are held by many people.

Stories of people losing their life savings overnight are all too common, and there have even been cases of people committing suicide in the aftermath of a crypto crash.

Clearly, this is not an ideal scenario- but all too common as people invest what they cannot afford to lose only to watch it vanish into nothing in a bear market.

So is there a better way to manage token values, such that death spirals become rarer, if not eliminated altogether?

Understanding the process of a death spiral

In order to eliminate death spirals, it is first necessary to understand what causes the death spiral in the first place.

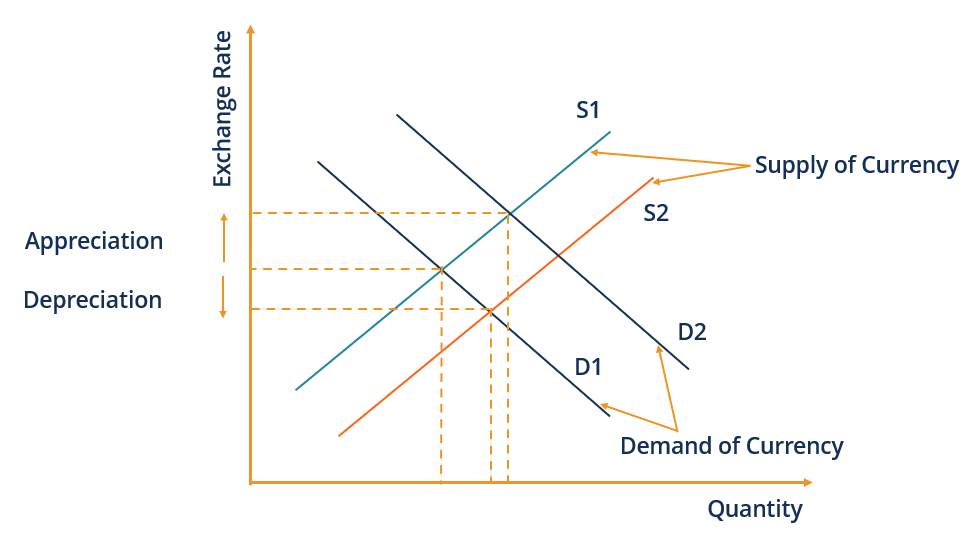

I have previously discussed how supply and demand of tokens influences price.

But what happens during a death spiral is a unique combination of fear and inflated token prices that drives people to make selfish decisions. Since everyone is cognizant that everyone else knows that the token is overvalued and that a devaluation is likely to occur, all holders are likely on high alert for when the first signs of devaluation occur.

Once it starts, everyone begins to sell, and no one wants to buy. This results in a massive increase in supply, while demand falls, with rapidly decreasing token prices being the result.

And in the crypto world, where there is no lender of last resort to provide emergency liquidity and funding, a death spiral may very well be irreversible, or at the very least, difficult to stop.

Since Luna’s all-time high of US$116 last June, it has since crashed, and has never recovered. It first began with rumours of an imminent depeg of UST from the USD, and when the first sign of such a depeg began to show, holders dumped all of the Luna they were holding, and converted what UST they held into other currencies.

And Luna is not the only one that is vulnerable to such an issue. Any token that fails to collateralise itself properly leaves itself in a risky position, where even the slightest bit of fear can trigger the start of mass selloffs and the beginning of a death spiral.

In short, a death spiral occurs when people expect the price of a token to drop, and are prepared to sell at the first sign of trouble.

Demand and supply manipulation

Of course, if demand and supply are the cause of the death spiral, a very natural response will be to try and manipulate the demand and supply of tokens, and this is exactly what many stablecoins do.

Collateral accumulation and management is merely a way of influencing demand and supply of tokens. Full reserve stablecoins like USDC for example, issue the same amount of stablecoins for an equivalent value in USD that they receive. In this way, as demand rises, supply also rises to keep the price of 1 USDC token equal to 1 USD.

Conversely, when demand for USDC falls and pushes the value of USDC downwards, Circle’s customers sell their tokens, and Circle refunds them in USD while burning the tokens- meaning that supply also falls with demand and price is kept stable.

Of course, the natural limitation of this is that large amounts of reserves are often necessary to keep the price of the stablecoin tokens stable.

Algorithmic stablecoins like Terra and Luna employ a different strategy to avoid having to keep large amounts of collateral. How the Terra ecosystem worked was that Terra would be collateralised with Luna, and traders could arbitrage between the two tokens freely until 1 UST token was worth exactly 1 USD. In this way, Terra could function without having to hold large amounts of collateral.

But collateralisation is not the only way that companies can manipulate demand and supply. Stablecoins have an interest in maintaining a currency peg, but companies who launch their own non-stablecoin tokens often have an interest in increasing the price of their own tokens.

Demand for a token is often a mix between transactional demand, in which people buy a particular token because it can be used in transactions, demand for a currency to hold on to in case of emergency (as opposed to say, holding on to other non-currency assets), and a speculative demand for the token.

Companies may increase the transactional demand for the token by convincing merchants to accept it as a form of payment, but quite often, there is a process of hyping up a token or project that results in many more people buying the token for speculative reasons rather than from a desire to use it for transactions.

In these cases, the company in question often also holds large amounts of the token that they create, because an inflated token price will mean that they have more money, at least on paper.

But while this works for a bull market because everyone is driven by greed, the speculative demand comes back to bite during a bear market, when fear is the dominant sentiment.

Tokenomics during a downturn

Because bull market incentives do not work during a bear market, a different set of policies and strategies are needed.

The first, and most obvious, is to try and isolate the token in question from the prevailing sentiment- often by creating demand and therefore confidence in the token. Bank loans and bailouts are the clearest manifestation of such a strategy.

Once a company gets the cash injection, panicking investors may see that there are still others who are willing to back the token and hold on to it, and therefore also decide to hold on to their share of tokens.

But in the crypto world, this strategy may not always work- especially for companies that have a large amount of their tokens being held by consumers. Once consumers start stampeding for the exit, there may not be enough time to secure a deal before the death spiral takes its toll.

Speeding up this process is possible, but it also means that banks or some other institution must keep large amounts of cash on hand in order to be able to bail out companies that are threatened by a death spiral- and this would involve some form of centralised decision making which goes against the decentralised ethos of the crypto world.

As such, companies will often try their best to use what assets they have to shore up their token price and reassure their holders that the token price can, in fact, hold up.

Unfortunately, because a significant portion of the company’s assets are also often in their native token, selling these tokens is likely to bring about the very same death spiral that they are trying to avoid.

Demand-based solutions, therefore, are clumsy and quite limited- but supply-side solutions are often yet to be explored.

And this is where the inspiration can be taken from stablecoins.

Stablecoins do not wait for excess demand to come back and bite before they take action- instead, part of why stablecoins remain stable even in times of crisis is because they scale supply up and down with demand, regardless of whether it is a bear market or a bull market.

While collateralisation is often the strategy for stablecoins, this is not as applicable to other tokens.

However, many companies still do keep a treasury of their own tokens, as well as other blue chip tokens- and this can be used.

Instead of selling their native token, however, there is a way to make it more scarce. The easiest way to do so is to burn large amounts of such tokens, and thereby reduce the available supply of tokens on the market.

This may, however, mean that the company loses much of its assets, and it risks having its balance sheet fall into the red- an unpalatable situation. Yet, it should still be a plan worth considering because the alternative is for holders to sell anyway, and for the company to be left with worthless tokens anyway.

In this way, the company may at least preserve some sense of solidarity, and buy itself some much-needed time to secure additional funding, with which it can use to stimulate demand.

A less risky option may be available for proof-of-stake blockchains, where tokens can be staked and therefore locked away. While it may not be as effective as burning tokens outright, since derivatives of staked assets may still be available for trading, it may at least assure holders that the company does not intend to dump its bag of tokens and leave them holding worthless tokens.

In both cases, what is paramount is to maintain the support of the community- since they likely represent the largest group of holders aside from the company itself. Without such support, however temporary it may be, death spirals may be entirely unavoidable.

Death spirals have claimed many different tokens- but they are not unstoppable, at least in theory. But it will require some unique thinking and financial engineering in order to find a good solution moving forward- one that maintains the decentralised ethos of the crypto world while allowing for flexible and quick responses to crises.

Disclaimer: The information provided is not trading advice, Bitcoinworld.co.in holds no liability for any investments made based on the information provided on this page. We strongly recommend independent research and/or consultation with a qualified professional before making any investment decisions.