Last week, the crypto world was rocked by significant developments as the US Securities and Exchange Commission (SEC) filed lawsuits against two of the industry’s giants: Binance and Coinbase. The charges? Operating as unlicensed securities exchanges. If that wasn’t enough, Binance is also facing a separate lawsuit from the Commodities and Futures Trading Commission (CFTC), alleging the operation of an illegal digital asset derivatives exchange. For many within the crypto ecosystem, these actions raise a critical question: why does the classification of crypto as a security or commodity even matter? Is it truly significant if it’s one versus the other? And why can’t cryptocurrency simply be considered a currency, akin to the Euro or the Japanese Yen?

For the average crypto user, these regulatory nuances might seem abstract. After all, you don’t necessarily need to grasp the legal distinctions to trade or transact in crypto. However, as regulators intensify their scrutiny of exchanges like Binance and Coinbase, this disconnect might not last for long. Lawsuits targeting major exchanges with millions of users are bound to have ripple effects, impacting both their clientele and partners.

Securities vs. Commodities: What’s the Real Difference?

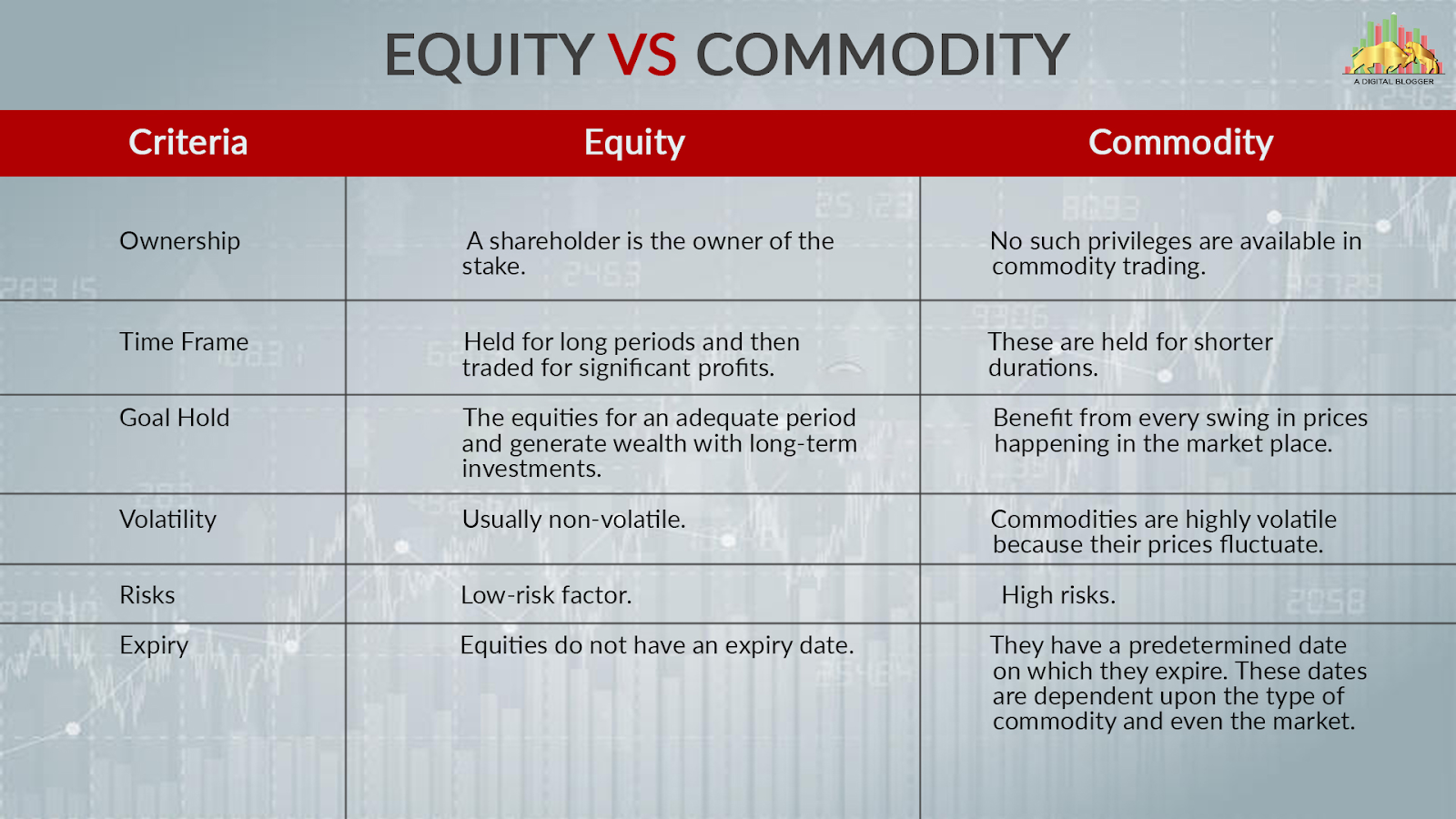

While the terms ‘securities’ and ‘commodities’ might sound like interchangeable investment jargon, there’s a crucial legal difference. Think of it this way:

- Securities: These are financial instruments representing ownership or debt in a company. Think of stocks – when you buy a share, you have a claim on a portion of that company.

- Commodities: These are raw materials or primary agricultural products that can be bought or sold. Examples include oil, gold, or agricultural products.

The expectation of profit differs too. If you buy securities, your profit is often tied to the success of the company issuing them. For instance, if Ripple performs well, the value of its XRP token could increase. The SEC argues that this expectation of profit based on the efforts of others makes XRP an investment contract, a determination based on the well-known Howey Test. This test is the SEC’s primary tool for classifying cryptocurrencies as securities and thus falling under their regulatory purview.

Commodities, on the other hand, generate profit when the price of the commodity itself goes up. You don’t expect dividends from the oil producer; you profit if the price of oil increases.

For everyday users and retail investors, this distinction might seem academic. You likely won’t need to dissect these legal definitions for your day-to-day crypto activities. However, this classification is paramount for companies like Binance and Coinbase. They need specific licenses to list securities or operate exchanges dealing with them.

Crypto Accounting: Asset, Liability, or Equity? The Murky Waters

The security vs. commodity debate isn’t the only classification challenge facing crypto. Accounting for crypto assets adds another layer of complexity.

Public companies are required to publish annual financial statements, including balance sheets, income statements, and cash flow statements. But how exactly should crypto assets be accounted for? Karthik Rajeswaran from Headquarters highlighted these challenges in his keynote speech at Crypto Expo Asia 2023:

“Firstly, there is the issue of volatility. The price of crypto assets are volatile, and can change drastically. Should we value them at the present market rate? And how should we do so? Different exchanges may see different tokens trade at different points, so which price point should be taken as the accurate one? And should we deal with the cost of acquiring crypto assets, and how should we value crypto subsequently, after the crypto has been obtained?

Then there is also the issue of how complex many crypto assets are. Are NFTs assets? Should we treat crypto that is being staked as part of a Proof-of-Stake consensus mechanism in the same way as crypto that is not being staked?”

-Karthik Rajeswaran, Vice President of Product, Headquarters

Currently, clear guidelines are still evolving. The Financial Accounting Standards Board (FASB) has proposed treating crypto as an indefinite-lived intangible asset. This means it won’t be subject to amortization or depreciation but will need to be tested for impairment. Interestingly, while decreases in value will be recognized, increases won’t be.

What are the implications of these rules?

- Potential Benefits: Financial debacles like the Terra/Luna collapse might be less likely, as companies couldn’t solely rely on ever-increasing token prices to demonstrate profitability.

- Potential Challenges: Financial statements might not fully reflect a company’s true financial standing if they hold significant crypto assets, as unrealized gains wouldn’t be shown.

Furthermore, the security vs. commodity classification directly impacts how crypto is listed on balance sheets. Securities, being investment contracts, would likely be classified as liabilities for the issuer. Commodities, on the other hand, are generally considered assets.

Is There a Smarter Way Forward for Crypto Regulation?

It’s easy to understand why retail investors might feel disconnected from these regulatory battles. But the outcomes will shape the future of crypto. Some jurisdictions, like Malaysia and Indonesia, have streamlined the process by designating their securities commissions as the primary regulatory bodies for cryptocurrencies.

The current situation in the US, with the SEC and CFTC seemingly vying for control, raises concerns. While their stated goal is consumer protection, their actions sometimes appear more focused on jurisdictional expansion than collaborative regulation. Ideally, some regulation, even if imperfect initially, is better than none. This allows for a framework to protect consumers while fostering innovation.

A Tale of Two Approaches: US vs. Asia

| Jurisdiction | Regulatory Approach | Key Characteristics |

|---|---|---|

| United States | Adversarial | Focus on enforcement actions, potential jurisdictional overlap between SEC and CFTC, slower progress. |

| Hong Kong & Singapore | Proactive & Collaborative | Drafting regulations with industry feedback, aiming for clarity and fostering innovation, faster progress. |

Hong Kong and Singapore are taking a more proactive approach, actively seeking feedback from industry leaders while drafting regulations. While rushing into regulation can have its downsides, a phased approach – implementing initial regulations and refining them based on experience – might be a more effective strategy.

The key is cooperation, not conflict. However, given the current political climate in the US, achieving such collaboration might be a significant hurdle.

Ultimately, defining crypto as a commodity or security is just one piece of the puzzle. We also need clear accounting standards and regulations that are fair to all stakeholders. Crypto regulation is still in its early stages, and the US approach, while assertive, isn’t the only model. The progress in Asian jurisdictions highlights the benefits of collaboration and a willingness to learn.

At its core, regulation should serve consumers and stakeholders. It’s not about winning a power struggle but about fostering a safe and innovative environment through cooperation and education.

Disclaimer: The information provided is not trading advice, Bitcoinworld.co.in holds no liability for any investments made based on the information provided on this page. We strongly recommend independent research and/or consultation with a qualified professional before making any investment decisions.