For years, the crypto community has echoed a bold claim: cryptocurrencies and blockchain are set to revolutionize the world. It’s a powerful vision, isn’t it? Imagine a financial system unshackled from government control, offering true freedom and equity. The promise of blockchain was revolutionary – a chance to break free from inflation-driving governments and corporations perceived as wealth extractors. A bigger, more evenly distributed pie for everyone – that was the dream.

The Libertarian Roots of Crypto

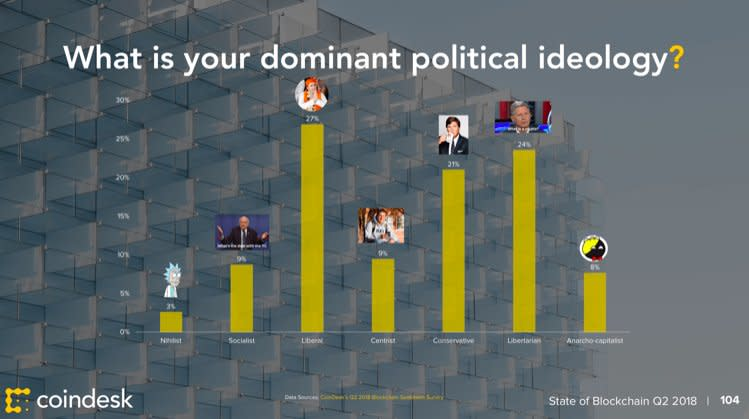

This ideology definitely fueled the early crypto boom. Think back to the pioneers – figures like Roger Ver, who openly linked their crypto enthusiasm to libertarian ideals. Remember that 2018 Coindesk survey? It revealed that a significant chunk of crypto holders leaned right: 21% conservative, 24% libertarian, and even 8% anarcho-capitalist. That’s a majority with a clear vision of financial freedom.

Even today, those echoes persist. Look at Texas, a conservative stronghold, becoming a crypto-friendly state. Republican lawmakers are often seen as pro-crypto, while figures like Elizabeth Warren are rallying against it.

But here’s the crucial question: Is crypto truly equipped to reshape the global order? Take a closer look, and you might find that the crypto world mirrors the traditional world in surprising ways. It might even, ironically, offer governments and corporations *more* control.

Central Banks Reimagined? The Commercialization of Power

Central banks and governments – often seen as the villains in the crypto narrative. Decentralization is crypto’s mantra, while central banks represent, well, centralization. Crypto libertarians argue that central bank regulations stifle free markets and create inefficiencies. For many in crypto, a world without central banks is a promised land.

But let’s be realistic. Even in a crypto-centric world, monetary policy is still essential. Someone needs to make decisions: When to issue more currency? How should it be distributed? Crypto’s answer so far? Democratization. Decentralized decision-making, where individuals vote based on their own interests.

There’s a theoretical appeal to this – the idea that the collective wisdom of the people leads to the best outcomes. But crypto voting isn’t the democratic ideal we know. It’s less “one person, one vote” and more “one token, one vote.” It’s closer to corporate voting, where money can indeed buy influence.

Remember the Luna crash? Do Kwon’s Luna Foundation Guard effectively pushed through a blockchain revival vote by controlling a massive chunk of tokens – around 60% of the circulation.

This raises a critical question: Is tyranny by elected governments really so different from tyranny by wealthy elites – plutocrats? Probably not. And if self-interest drives behavior, what prevents crypto democracies from sliding into plutocracies? Power tends to accumulate, and those without power often remain powerless.

In the traditional world, governments are (at least theoretically) accountable to the people. Wealth redistribution policies can gain traction when inequality becomes too extreme, as governments need public support to stay in power. But in crypto, why would the powerful willingly redistribute power to the masses, especially when there’s no direct incentive to do so?

Oligarchs, Old and New: Meet the Crypto Elite

Beyond governance, crypto promised to dismantle old, rent-seeking oligarchies and usher in fairer wealth distribution. Nikita Khrushchev famously quipped, “economics is a subject that does not greatly respect one’s wishes.” Irony aside, there’s truth in that.

The Web3 landscape isn’t exactly a picture of perfect competition. In almost every crypto market, a few dominant players emerge, controlling the lion’s share while smaller entities scrap for the rest.

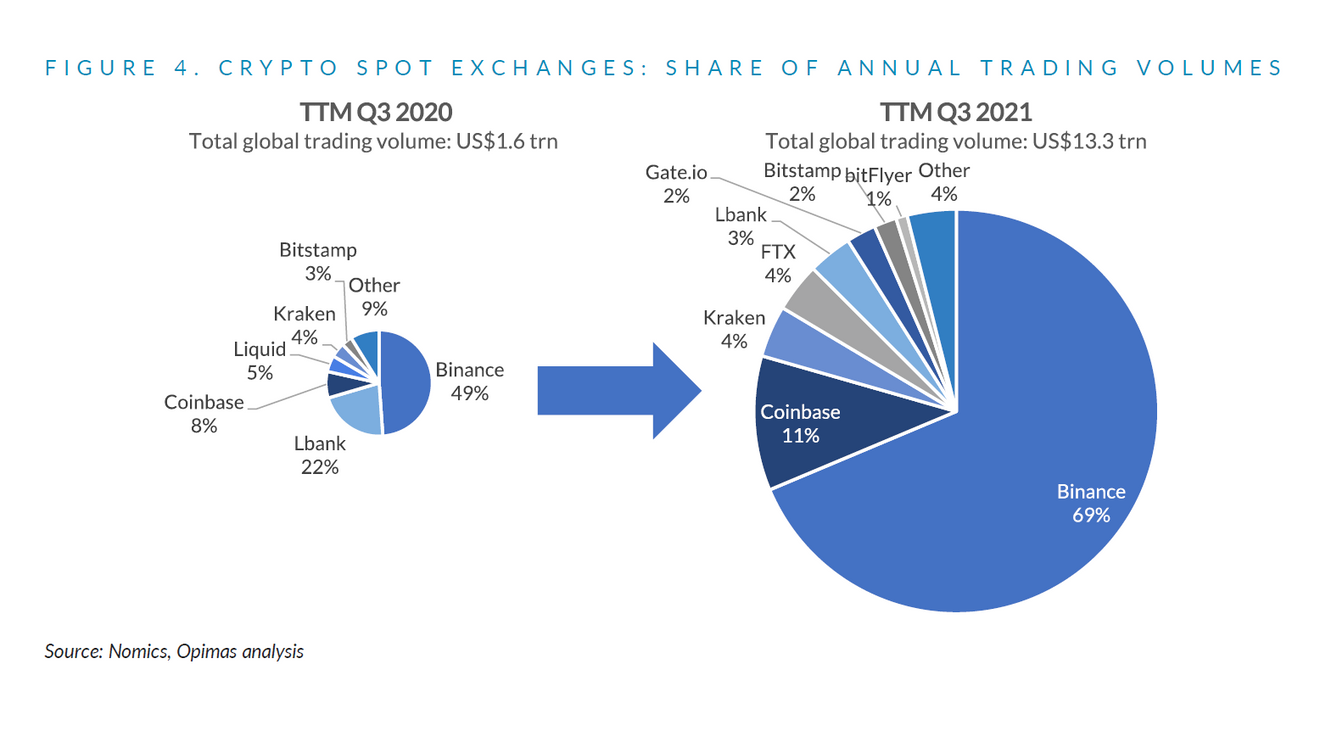

Consider crypto exchanges. Binance is the undisputed king.

Its trading volume dwarfs competitors, giving it immense market control.

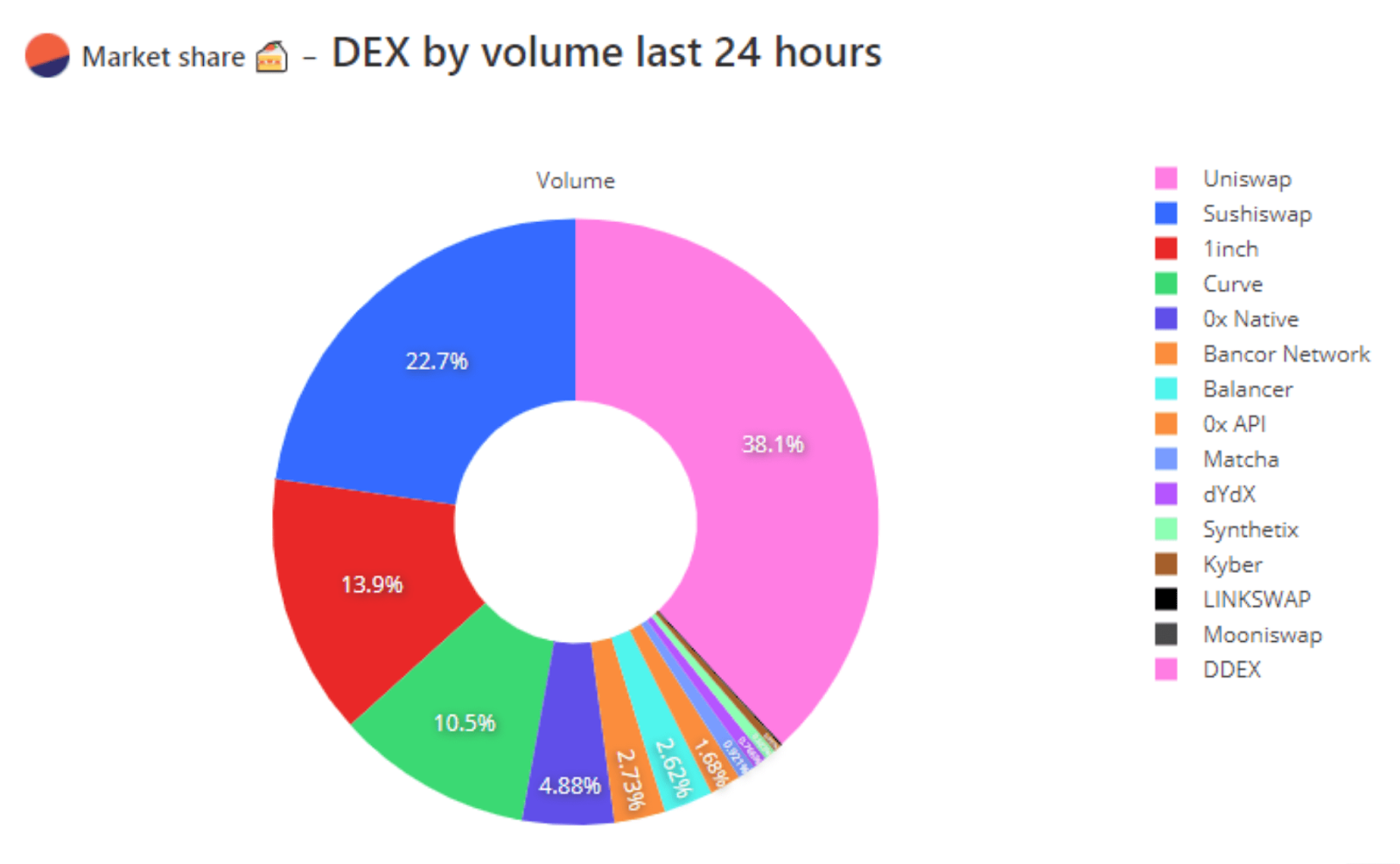

DeFi isn’t much different. The top four players control roughly 85% of the market.

And the NFT marketplace battle is heating up between OpenSea and Blur.

So, is crypto eliminating monopolies and oligopolies? Not really. It seems to be creating new ones as new markets emerge. Is there a fundamental difference between traditional and crypto oligopolies? Probably not. Customers gravitate towards companies they perceive as the best. The most successful companies gain market share, and oligopolies form naturally through competition. It’s not necessarily about government manipulation or corporate greed; it’s often a natural outcome of market dynamics, whether in the real world or the crypto realm.

Crypto Crime: A Professional Enterprise

Every world order has its dark side. For a technology promising transformation, crypto’s underbelly is surprisingly familiar.

In recent years, Russia and North Korea, both geopolitical outliers, have become hubs for crypto crime, though with distinct approaches.

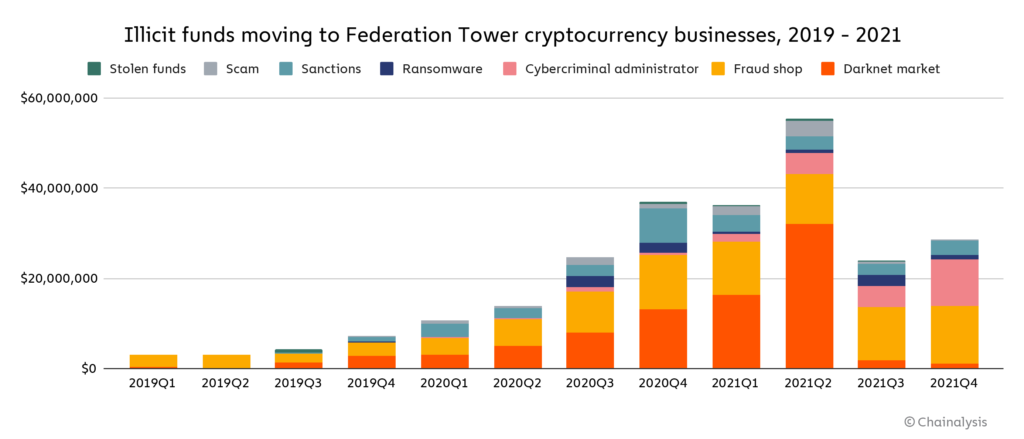

Russia’s history with financial crime, including money laundering, predates crypto. The country is also notorious for facilitating the illicit drug trade. With crypto, Russian criminals have upped their game. Chainalysis suggests that the Russian government, if not actively involved, is at least turning a blind eye. Ransomware and crypto hack proceeds increasingly flow into Russia, notably to locations like Federation Tower in Moscow.

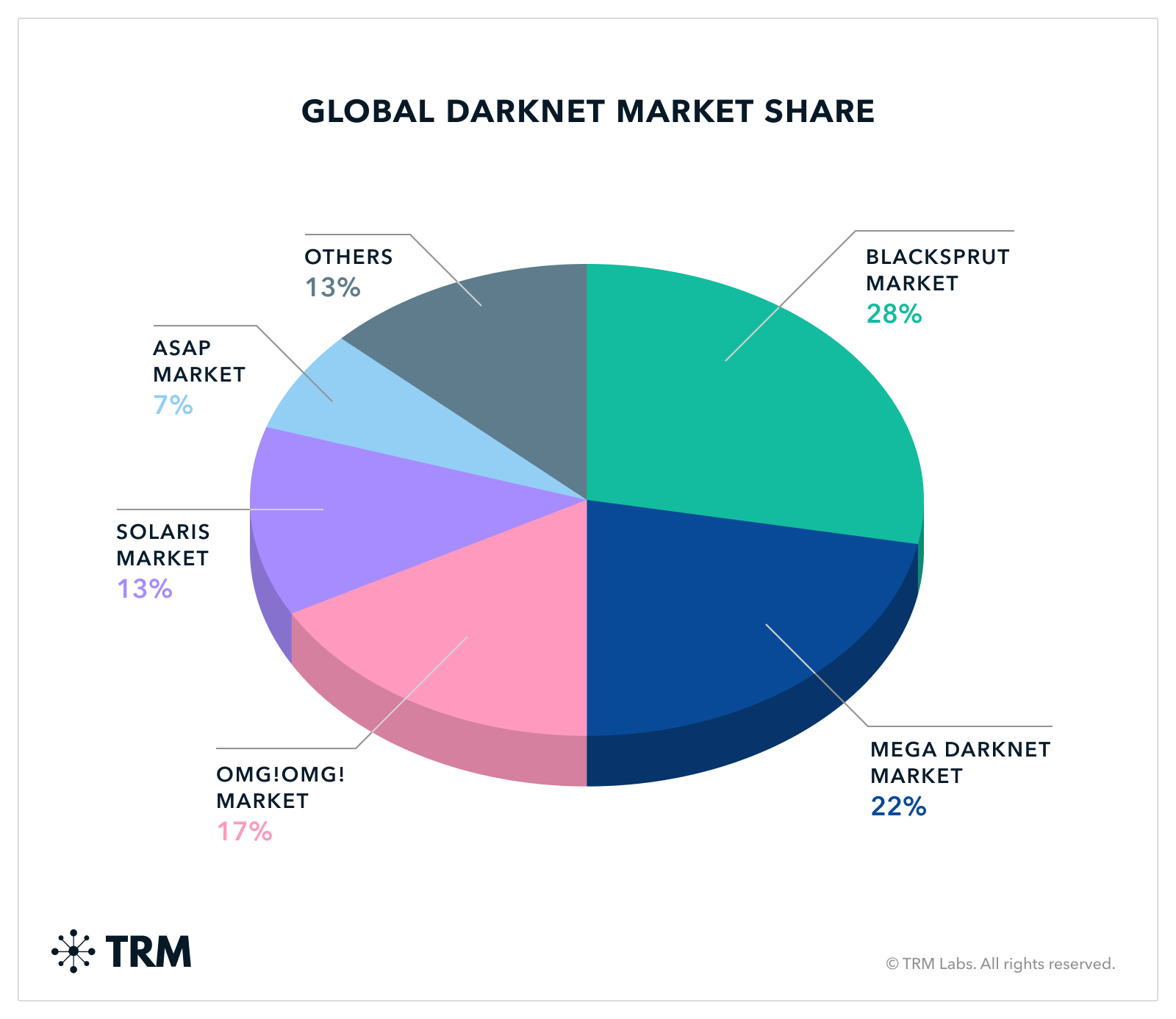

Crypto has transformed financial crime in Russia. Hydra, the darknet marketplace dismantled last year, operated primarily from Russia. Even after the takedown, the same criminal networks persist, migrating to other darknet platforms.

North Korea takes it further. While Russia might be passively benefiting from crypto crime, North Korea is actively engaged. Just recently, North Korean hackers allegedly stole $100 million from Atomic Wallet, attempting to launder funds through Garantex. These attacks are linked to the Lazarus Group, believed to be backed by the North Korean government.

This is just the tip of the iceberg. Lazarus is suspected in the Bangladesh Bank heist ($81 million), attacks on Banco del Austro in Ecuador ($12 million), and Tien Phong Bank in Vietnam ($1 million). Turning a blind eye to crime is one thing; state-sponsored cyber theft targeting foreign financial institutions is another level entirely. Yet, this is North Korea’s reality.

Crypto’s Mark, Not a Revolution

Has crypto fundamentally altered international relations or the world order? Not in a revolutionary sense. Threats to individual freedom persist, and states adapt new technologies to serve existing power dynamics, just as they always have.

Does this mean crypto won’t reshape the world order? Perhaps not in the radical way initially envisioned. Crypto hasn’t yet delivered on promises of sweeping global change for everyone. But it *has* undeniably impacted global finance.

Adoption is growing, and traditional finance is paying attention. However, it’s time to adjust expectations. Crypto hasn’t created a completely new world order. Instead, it often reflects and reinforces existing patterns – in market structures, international relations, and even the dynamics of power and influence.